What are the key financial reports?

The three major financial statement reports are the balance sheet, income statement, and statement of cash flows.

For-profit businesses use four primary types of financial statement: the balance sheet, the income statement, the statement of cash flow, and the statement of retained earnings. Read on to explore each one and the information it conveys.

- Income statement.

- Cash flow statement.

- Statement of changes in equity.

- Balance sheet.

- Note to financial statements.

The income statement, balance sheet, and statement of cash flows are required financial statements.

- Balance sheets.

- Income statements.

- Cash flow statements.

- Statements of shareholders' equity.

The balance sheet, income statement, and cash flow statement each offer unique details with information that is all interconnected. Together the three statements give a comprehensive portrayal of the company's operating activities.

Although the guidelines for accountants are extensive, there are five main principles that underpin accounting practices and the preparation of financial statements. These are the accrual principle, the matching principle, the historic cost principle, the conservatism principle and the principle of substance over form.

The four financial statements (in order of preparation) are the income statement, statement of retained earnings (or statement of shareholders' equity), balance sheet, and statement of cash flows.

- 3.1. Balance Sheet.

- 3.2. Income Statement.

- 3.3. Cash Flow Statement.

- 3.4. Statement of Changes in Capital.

- 3.5. Notes to Financial Statements.

The income statement will be the most important if you want to evaluate a business's performance or ascertain your tax liability. The income statement (Profit and loss account) measures and reports how much profit a business has generated over time.

Which financial statement is most important to CEO?

The cash flow statement accounts for the money flowing into and out of a business over a specified period of time. The cash flow statement is arguably the most important of these financial reports because it reveals a business's actual ability to operate.

Financial reports show historical data, but they provide insight into how a business spends its profits, whether they are reinvested into the business, and whether the company can sustain future growth. Operational reports provide business intelligence on how efficiently a company performs.

The three main financial statements are the balance sheet, income statement, and cash flow statement. Chief Financial Officers (CFOs) must understand what information each statement provides and how they are interrelated.

The standard requires a complete set of financial statements to comprise a statement of financial position, a statement of profit or loss and other comprehensive income, a statement of changes in equity and a statement of cash flows.

The three golden rules of accounting are (1) debit all expenses and losses, credit all incomes and gains, (2) debit the receiver, credit the giver, and (3) debit what comes in, credit what goes out.

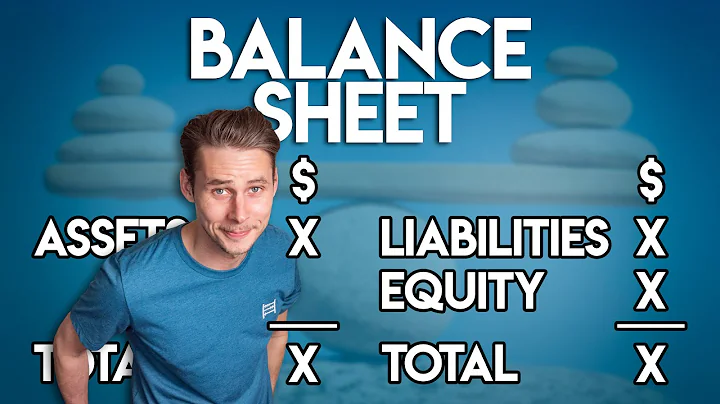

A company's balance sheet is comprised of assets, liabilities, and equity. Assets represent things of value that a company owns and has in its possession, or something that will be received and can be measured objectively.

What is a 3-Statement Model? In financial modeling, the “3 statements” refer to the Income Statement, Balance Sheet, and Cash Flow Statement. Collectively, these show you a company's revenue, expenses, cash, debt, equity, and cash flow over time, and you can use them to determine why these items have changed.

Note: The 4 C's is defined as Chart of Accounts, Calendar, Currency, and accounting Convention.

So, here the students are going to learn about these 3 fundamental accounting assumptions which are known as Going Concern, Consistency, and Accrual.

Traditionally, each account in the COA is numbered, and accountants can quickly identify its type by the first digit. For example, asset accounts for larger businesses are generally numbered 1000 to 1999 (or 100 to 199), and liabilities are generally numbered 2000 to 2999 (or 200 to 299).

Is A common stock an asset?

Common stock is an asset for the company that issued it, but it is not a liability. Common stock represents ownership in a company and represents a claim on the company's assets and earnings.

- Step 1: gather all relevant financial data. ...

- Step 2: categorize and organize the data. ...

- Step 3: draft preliminary financial statements. ...

- Step 4: review and reconcile all data. ...

- Step 5: finalize and report.

The balance sheet provides information on a company's resources (assets) and its sources of capital (equity and liabilities/debt). This information helps an analyst assess a company's ability to pay for its near-term operating needs, meet future debt obligations, and make distributions to owners.

Income statement: This is the first financial statement prepared. The income statement is prepared to look at a company's revenues and expenses over a certain period, such as a month, a quarter, or a year.

Generally accepted accounting principles, or GAAP, are standards that encompass the details, complexities, and legalities of business and corporate accounting. The Financial Accounting Standards Board (FASB) uses GAAP as the foundation for its comprehensive set of approved accounting methods and practices.